Mortgage crisis deepens as one in four face missing payments this year

An estimated 1.6 million households face spiralling debts as they are hit by huge hikes in interest rates

A quarter of Britain’s mortgage holders face missing their payments by the end of this year as interest rates continue to soar, analysis shows – with thousands told already that they could lose their homes.

Some 1.6 million homeowners will come to the end of their fixed-rate deals this year, with an average hike of about £1,800 annually on their repayments as they move on to higher interest rates.

Since the actions of Liz Truss as prime minister in 2022 sent rates spiralling, charities say pleas for financial assistance have tripled.

The latest figures from the Ministry of Justice show that 5,182 repossession claims were made in England and Wales in the first quarter of this year, an increase of more than 40 per cent in just 18 months.

Have you fallen into arrears with your mortgage payments? Email holly.evans@independent.co.uk

Jane Tully, of the Money Advice Trust, the charity behind National Debtline, said: “These are really challenging times for many mortgage holders as interest rates remain high and cost of living pressures continue.

“For those coming to the end of fixed-rate deals, the financial shock will be significant as monthly repayments rise sharply. People often prioritise housing costs above other bills, and we are seeing the impact at National Debtline, with more mortgage holders now contacting us for help.”

The Bank of England’s latest figures show that the value of outstanding mortgage balances with arrears now stands at £20.3bn, which is 50.3 per cent higher than in 2022.

Analysts at investment firm Hargreaves Lansdown calculated that the mortgage repayments of 2.1 million homeowners – one in four – will exceed 25 per cent of their disposable income by the end of this year, putting them at risk of arrears.

Around 390,000 of those households are deemed to be at “critical risk”, meaning they have inadequate savings with unsustainable spending and are being pushed further into a negative budget.

Sarah Coles, of Hargreaves Lansdown, said: “We look at what people have in addition to their homes and their broader finances. The risk is increasing that people don’t have savings to fall back on.”

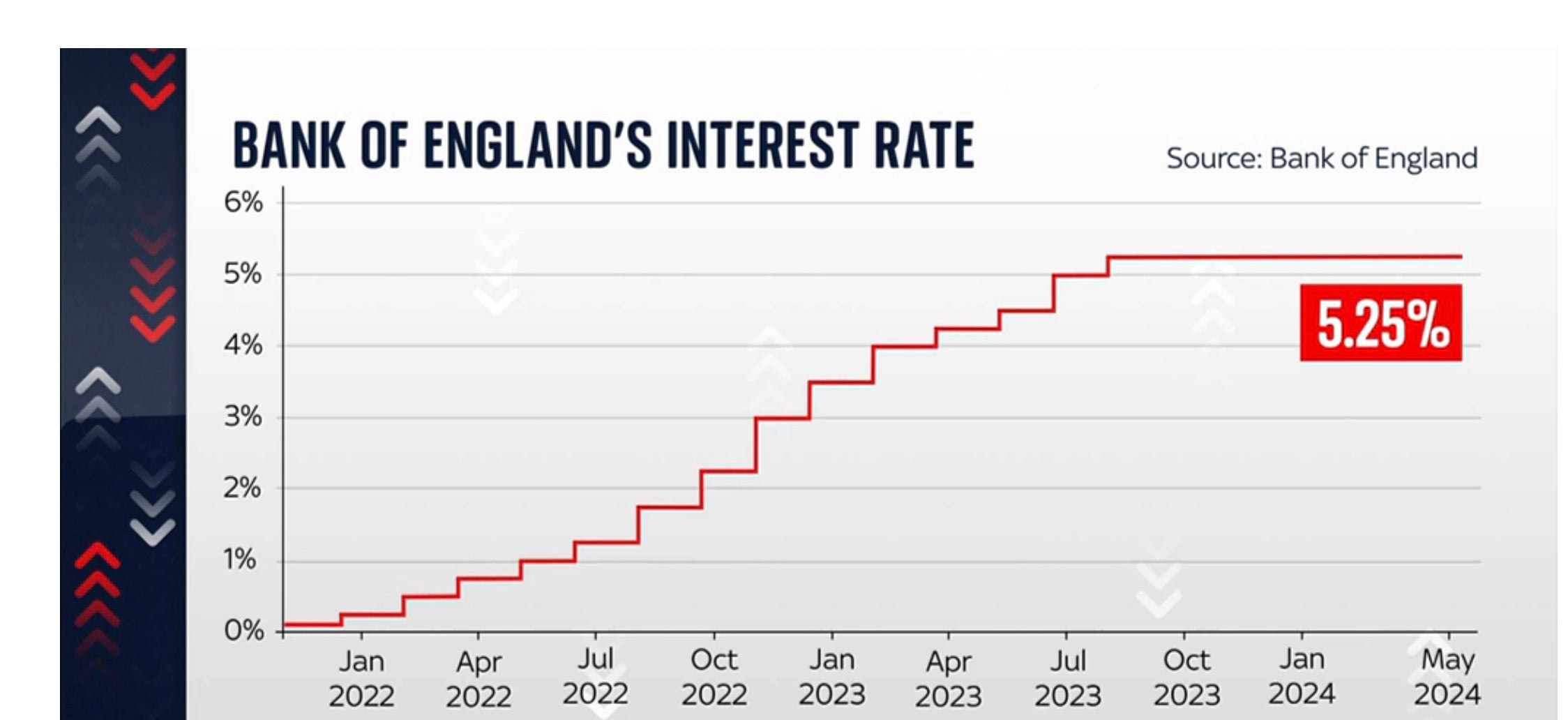

The Bank of England interest rate remains at a 16-year high of 5.25 per cent, with rising inflation partly caused by fallout from the pandemic and the war in Ukraine. Those moving from low fixed-term deals now face rates of around 7 per cent.

Last year the government introduced the Mortgage Charter, which prevents banks from progressing repossession proceedings following initial non-payment, but the scheme is up for review in July, after the general election.

One mortgage adviser said the crisis has led a significant number of people to borrow more, with a heavy reliance on credit cards and personal loans to balance household budgets.

“Homeowners are now facing tough decisions, such as cutting back on other expenses, seeking mortgage renegotiations, or, in the more severe cases, considering selling their homes to avoid repossession,” said Pete Mugleston of Online Mortgage Advisor.

Interest rates are predicted to improve later this year, with the International Monetary Fund recommending that they should fall to 3.5 per cent by the end of 2025.

Yet for those struggling to make ends meet, the situation has only worsened in recent months, with the cost of living crisis expected to be at the forefront of both Labour and Conservative campaigning ahead of the election on 4 July.

“I think we’ve weathered the storm so far, which is positive, and we are expecting rates to start coming down in earnest later this year, which is also positive,” Ms Coles said. “If you are in arrears, things will get worse for a bit, but there is real hope that things will eventually start getting better.”

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks