How inflation announcement could affect your mortgage

Brokers hail ‘welcome news’ on inflation figures – but remain cautious about impact on interest rates

It’s been a turbulent few days for prospective and current homeowners looking for mortgages, with several major lenders announcing increases in rates after a period of decline in borrowing costs.

Nationwide, the country’s biggest building society, revealed its mortgage rates would rise by up to 0.25 percentage points on Tuesday. It came after lenders Halifax and TSB said they were also raising rates on some of their products.

But, strangely, other lenders had gone in the other direction, with Santander announcing mortgage rate cuts of 0.16 percentage points.

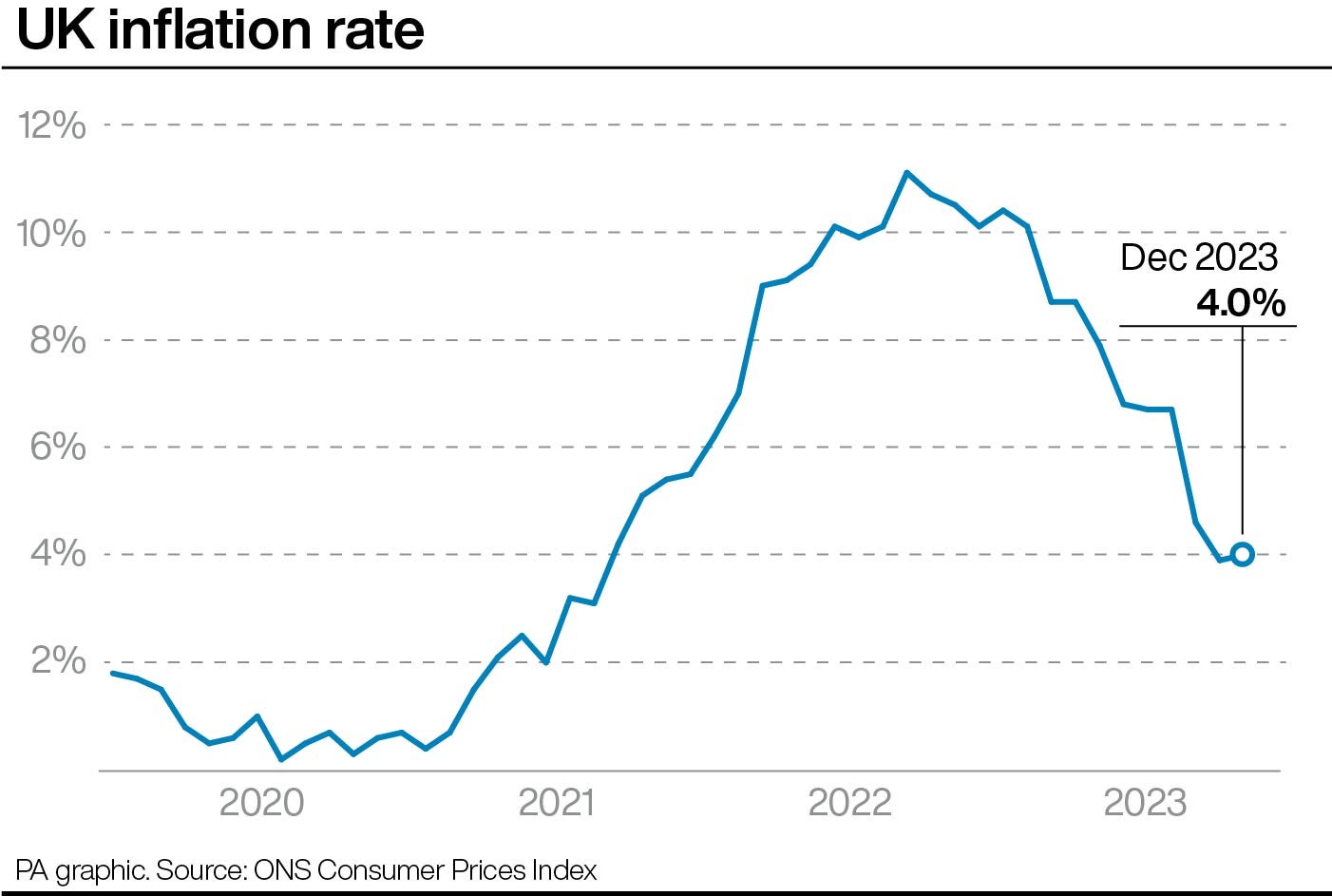

The mixed picture for rates comes after the Bank of England held its base rate at 5.25 per cent earlier this month. However, it was fears over Wednesday’s inflation figures which appear to have resulted in what some brokers are calling a “yo-yo” market.

Annual inflation up to December was 4 per cent, up from 3.9 per cent up to November. While initial fears that the figure for January could have been even higher led some lenders to “protect themselves” with their rate rises, the data published on Wednesday instead showed the rate had remained steady – providing some relief to homeowners.

Here we take a look at everything you need to know.

Why had mortgage rates gone up?

Mortgage rates are closely tied to swap rates, which is effectively the rate the lenders pay a financial institution for funding, and that is affected by the Bank of England’s base interest rate and inflation.

Experts had been predicting that inflation would go up marginally from the annual 4 per cent recorded last month, causing some lenders to “safeguard” themselves by hiking their own rates early, Ken James, director at Contractor Mortgage Services, told The Independent.

But with the figures instead showing the “welcome news” that inflation remained steady in January, Imran Hussain, director at Harmony Financial Services said this would hopefully “put a halt to mortgage rates edging up slightly and being so volatile, offering some stability to borrowers”.

Katy Eatenton, of Lifetime Wealth Management, was similarly optimistic, saying: “Mortgage rates and swap rates have been edging up over the past couple of weeks, so hopefully this will help stabilise things and encourage lenders to start pricing downwards again.”

What is the impact of inflation?

Inflation directly impacts the swap rate charged to lenders – and so they will pass it on to customers in the mortgage rates they charge.

The Bank of England also raises its base interest rate to try to curb inflation. As a result, the Bank has opted in recent months to keep its base rate relatively high, at 5.25 per cent – up from a low of just 0.1 per cent in March 2020 – which has left homeowners struggling to pay higher interest rates on their mortgages.

While Bank of England governor Andrew Bailey predicted the inflation rate could temporarily hit the hallowed target 2 per cent in the spring, economists are not forecasting a fall in the Bank’s base interest rate just yet.

What do Wednesday’s figures mean for interest rates?

While UK inflation is key to the Bank’s decision-making on whether to cut its base rate, offering relief for homeowners, there are many factors for its rate-setting Monetary Policy Committee to consider.

“This is certainly unexpected, and positive news, but on its own it won’t change the possibility that the Bank of England may hold rates higher for longer,” said Craig Fish, director at Lodestone Mortgages & Protection.

“Wages and employment data are just as important and if they look hotter than expected then an early rate cut is off the cards. The eyes of the MPC seem to be set on the Fed in the US, as it’s likely that when they make their first move (which could be a while) its likely that the UK will, too.”

This sentiment was echoed by Lewis Shaw, of Shaw Financial Services, who said: “It’s positive that inflation has remained at 4 per cent when many were expecting a rise; however, with US inflation rising, it means the likelihood of any base rate cut will be pushed back further.

“Furthermore, the hotter-than-expected US inflation caused Gilt yields to increase yesterday, meaning any further mortgage rate reductions will be paused, and we could see many lenders begin to reprice upwards.”

Advice for homeowners

With some mortgage rates rising ahead of the inflation figures on Wednesday, the market is volatile and homeowners on variable rates, or those coming off fixed rates, will be wondering if they should go for a new mortgage product with a rate, or stick at their lender’s variable rate in the hope that rates will go down later in the year.

Mr James said: “It varies from person to person ... are they on a variable rate because they are looking to sell, are they waiting for prices to fall and don’t want to lock into anything now because they feel the prices are high and they want to see if they can get a cheaper deal? The downside to that is whilst they are sitting on the fence, it’s costing them as the variable rates are extremely high.

“So the conversation we are having at the moment is is there a halfway house where they can mitigate the increase of the variable rate, but not getting stuck into a fix? The halfway house of course now is tracker rates, so a lot more people now are contemplating if tracker rates might be the right way to go. It’s not as cheap as a fixed but it’s not tied to a variable.

“Maybe go on a tracker rate and ride the storm and see where it takes us.”

How is the situation impacting house prices?

Despite the uncertainty over rates, brokers have insisted that the housing market remains buoyant. Earlier this month, Halifax reported that house prices in January were 2.5 per cent higher than the same month a year earlier.

But official data from the ONS on Wednesday suggested that average UK house price fell by 1.4 per cent in the 12 months to December, falling in value by an average of £4,000. In London, house prices fell by as much as 4.8 per cent, while in Scotland, they instead rose by 3.3 per cent.

Mr James said the current situation was a “nightmare” for people choosing the right mortgage product, but added that with rates not rising dramatically, it wasn’t putting people off buying homes.

He said: “Rates will start to reduce. And so we see demand, and demand is driving prices, and Halifax has given a couple of notices to say the market is starting to rise. I think demand is pushing that and I think the market is busy. The appetite is there, and people are wanting to move in for summer.”

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks