Greece debt crisis: The euro is a disaster even for the countries that do everything right

The euro is a capricious god, meting out punishment to sinners and saints alike

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.The euro might be worse for you than bankruptcy.

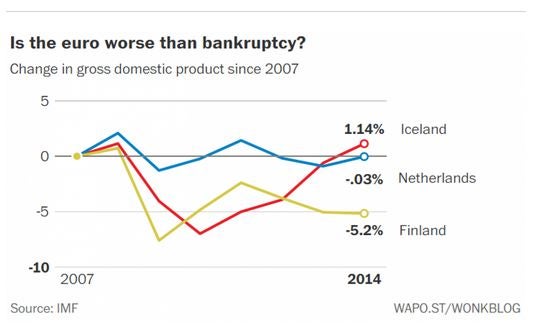

That, at least, has been the case for Finland and the Netherlands, which have actually grown less than Iceland has since 2007. Iceland, you might recall, basically went bankrupt in 2008.

Now, it's true that Finland and the Netherlands have had their fair share of economic problems, but those should have been manageable. Neither country is a basket case, and both have done what they were supposed to do. In other words, they've followed the rules, and the results have still been a catastrophe. That's because the euro itself is. Or, if you want to be polite, the common currency is "imperfect, and being imperfect is fragile, vulnerable, and doesn't deliver all the benefits it could." That was European Central Bank chief Mario Draghi's verdict on Thursday.

So what's happened to them? Well, just your run-of-the-mill bad economic news. It's only a slight exaggeration to say that Apple has kneecapped Finland's economy. Its two biggest exports were Nokia phones and paper products, but, as the country's former prime minister Alex Stubb has said, the iPhone killed the former and the iPad killed the latter. Now, the normal way to make up for this would be to cut costs by devaluing your currency, except that Finland doesn't have a currency to devalue anymore. It has the euro. So instead it's had to cut costs by cutting wages, which not only takes longer, but also causes more economic damage since you have to fire people to convince them to take pay cuts. The result has been a recession longer than anything in Finland's living memory, longer even than its great depression in the early 1990s. It hasn't helped, of course, that the rules of the euro zone have forced Finland's government to cut its budget at the same time that all this has been happening.

It's been a different kind of story in the Netherlands. Its goods are more than competitive abroad—its trade surplus is an absurd 10 percent of economic output—but its domestic spending is a problem. The Netherlands had a huge housing bubble, fueled, in part, by the fact that interest payments are fully tax deductible, that has since deflated some 20 percent. That's left Dutch households with a bigger debt burden than anyone else in the euro zone. On top of that, there's been the usual austerity to keep its recovery from being much—or any—of one. Indeed, the Netherlands' economy was slightly smaller at the end of 2014 than it was at the end of 2007. That's a lot better than Finland, whose economy has shrunk 5.2 percent during that time, but, as you can see below, it still lags the 1.1 percent growth Iceland has eked out.

Now, it's hard to do worse than Iceland. It basically turned its entire economy into a hedge fund that collapsed in 2008. Its banks defaulted, its government had to be bailed out, and its currency collapsed 60 percent. Not only that, but, between 2009 and 2014, Iceland did nearly twice as much austerity as the Netherlands and 12 times as much as Finland. And if that wasn't enough, Iceland's economic jeremiad also includes high household debt and capital controls that have prevented people from moving money out of the country and dissuaded them from moving it in.

But despite all this, Iceland has still managed to outperform Finland and the Netherlands. How is that possible? Well, it doesn't have the euro. It has its own currency, the krona. And as much as it hurt Iceland's people to lose 60 percent of their purchasing power on imported goods when the krona fell that much, it helped Iceland's economy by making their goods more competitive overseas. That was enough to keep what could have been a depression from turning into anything other than a bad recession.

The euro, though, does the opposite. Countries can't devalue their currencies or cut interest rates or even spend more when they get into trouble, and so they stay in trouble. All they can do is cut wages, cut spending, and then cut wages some more as penance for whatever economic transgressions they may or may not have committed. The euro straitjacket, in other words, turns ordinary problems into extraordinary ones (Finland) and extraordinary problems into historic ones (Greece). And that can happen whether or not you follow the rules.

The euro is a capricious god, meting out punishment to sinners and saints alike.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments