We are just starting to see the real impact of the oil price collapse

Economic View

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.As so often happens when a sea-change in financial flows occurs, it can take a long time before the full consequences become apparent. And so it is with the collapse of the oil price. We are now nearly a year on from that, yet it is only now that the news flow is picking up the hits being taken by the various players in the oil game. There is a further twist here. We are seeing the specific negatives, but we are not yet seeing the general positives. After any such shift there will be winners and losers, but so far it is the losers attracting the attention.

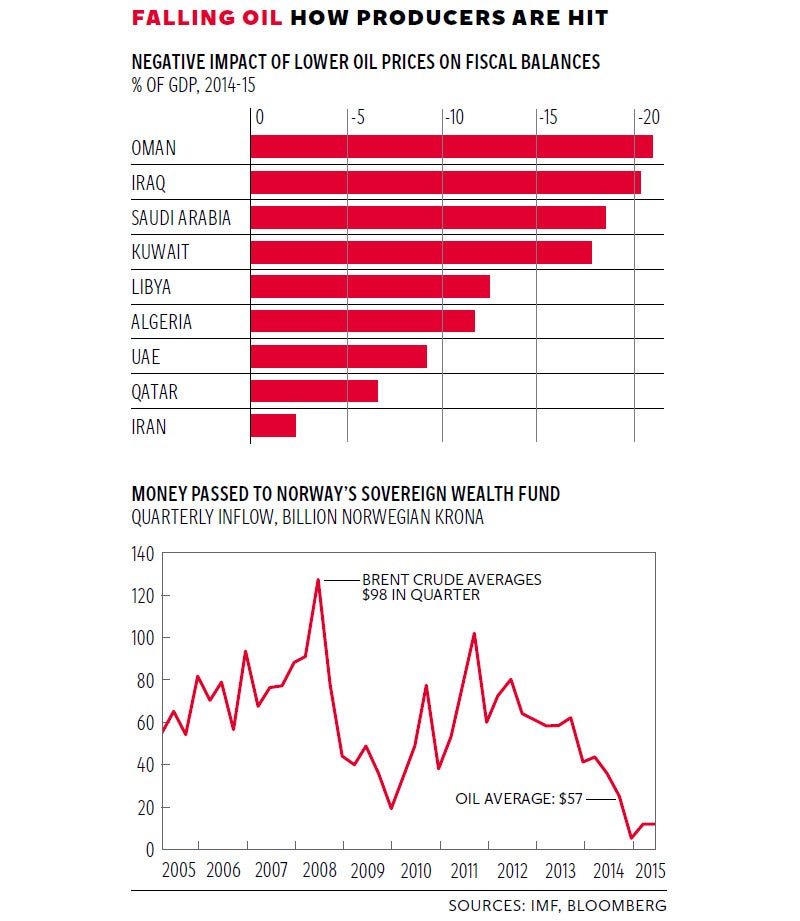

The graphs highlight two particular groups of losers: the countries that rely on oil revenues for a large part of their government income, and the sovereign wealth funds.

On the top is the impact on the fiscal position of a number of oil exporters, the percentage points by which the countries’ fiscal balance deteriorates as a result of the halving of the oil price. It comes from a new paper by the IMF on the regional economic outlook for the Middle East and Central Asia. As you would expect, all these oil producers take a hit, but for some it is worse than for others. For example Oman is more severely affected than the UAE. That is because the latter has a more diversified revenue base. However the report notes something else.

Oil importers, it says, “are benefiting from lower oil prices as well as economic reforms and improved euro area growth”.

It reckons that overall regional growth this year will be 2.5 per cent, half a percentage point below the IMF’s May 2015 projections. However, this will pick up to 4 per cent next year, supported by improved prospects for Iran and some recovery in oil exports. If that is right, well, 4 per cent growth is not bad, for it would be a lot faster than the developed world and probably above overall world growth next year. The main point here is that there is a particular and measurable negative impact on fiscal revenues, coupled with some damage to growth, but once that is taken into account, growth resumes at a decent level.

Now look at the impact on country finances, for most oil producing countries have the cushion of a sovereign wealth fund. The lower graph shows what has been happening to the largest fund of all, that of Norway. Its assets were down two quarters in a row, but that is thanks to the poor market conditions this year. While the flow into the fund varies with the oil price, as you would expect, it has remained positive – just – despite the collapse in the price. But Norway has been particularly disciplined about its oil revenues, maintaining the high tax levels common throughout Scandinavia, whereas most oil producing countries have relied on those revenues to finance current government spending. (Indeed the UK has spent its oil revenues, rather than setting them aside for future generations, so we have nothing to be proud about.)

So the practical questions for financial markets will be to what extent the sovereign wealth funds become net sellers of assets rather than net buyers, and what this will do to asset prices.

That is hard to answer because policy is still evolving and naturally will vary from country to country. The UAE seems reasonably upbeat, despite the fact that 65 per cent of its revenues comes from oil and gas. Its energy minister, Suhail Al Mazrouei, said at a conference in Abu Dhabi that major projects in the emirate would continue, including the new terminal at Abu Dhabi airport. And earlier this month Ali Al Mansoori, the chairman of Abu Dhabi’s Department of Economic Development, made the point to Bloomberg that an excessively high oil price was damaging too.

“It is a gift to the world that oil has dropped to $50,” he said. “Would we like for oil to stay at $50? Absolutely not. We would like oil to go to $70, $80, but beyond that I think it would hurt the economic growth.”

What I think we can assume is that the sovereign wealth funds, taken as a whole, will go from being a buyer of assets to a roughly neutral position. Some will continue to buy assets, particularly those that have not relied on oil and gas revenues. Singapore is the prime example here. Others will be net sellers, at least for a while.

Neutral overall would not be bad. It would be a force helping nudge up long-term interest rates, artificially depressed by QE, which would be fundamentally healthy for the world economy. As for other asset prices, it would at least take the froth off trophy assets, which would also be no bad thing.

As for the general boost to the world economy from cheaper raw materials, especially oil and gas, the calculations are still being made. The problem is that we have very little experience of two important phenomena.

One is a sudden plunge in the price. In the past prices have tended to rise sharply (hence the expression “oil shock”) but fall slowly. You can track through the consequences of cheaper energy, for oil and gas lead directly to lower food prices and indirectly to other price declines. All of these increase real output and raise living standards, but it is hard to put numbers on this – or rather you can put numbers on it but you cannot be sure how accurate those numbers may be.

The other is that we have no experience at all of a falling price boom – strong growth and solid increases in real living standards taking place as prices trend down rather than up. To get that you have to go back to the 19th century when conditions were so different that I’m not sure the experience is much use. A year from now, when the consequences of cheaper energy will have fed through the system, we will have more idea. Common sense says that cheaper energy – environmental issues aside – should be good for growth, and good growth ought ultimately to be good for the price of assets associated with that growth.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments