Hamish McRae: From the Brics to the Mints, is it time to take a new look at the emerging markets' success story?

Economic View: The developed world is now performing rather better and is producing good returns

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.There has been, in investment opinion at least, a switch of emphasis in the past few weeks. A year ago the general message was that growth would remain much stronger in the emerging economies than in the developed ones. Accordingly investment portfolios should switch emphasis towards the Brics, the Mints, and so on.

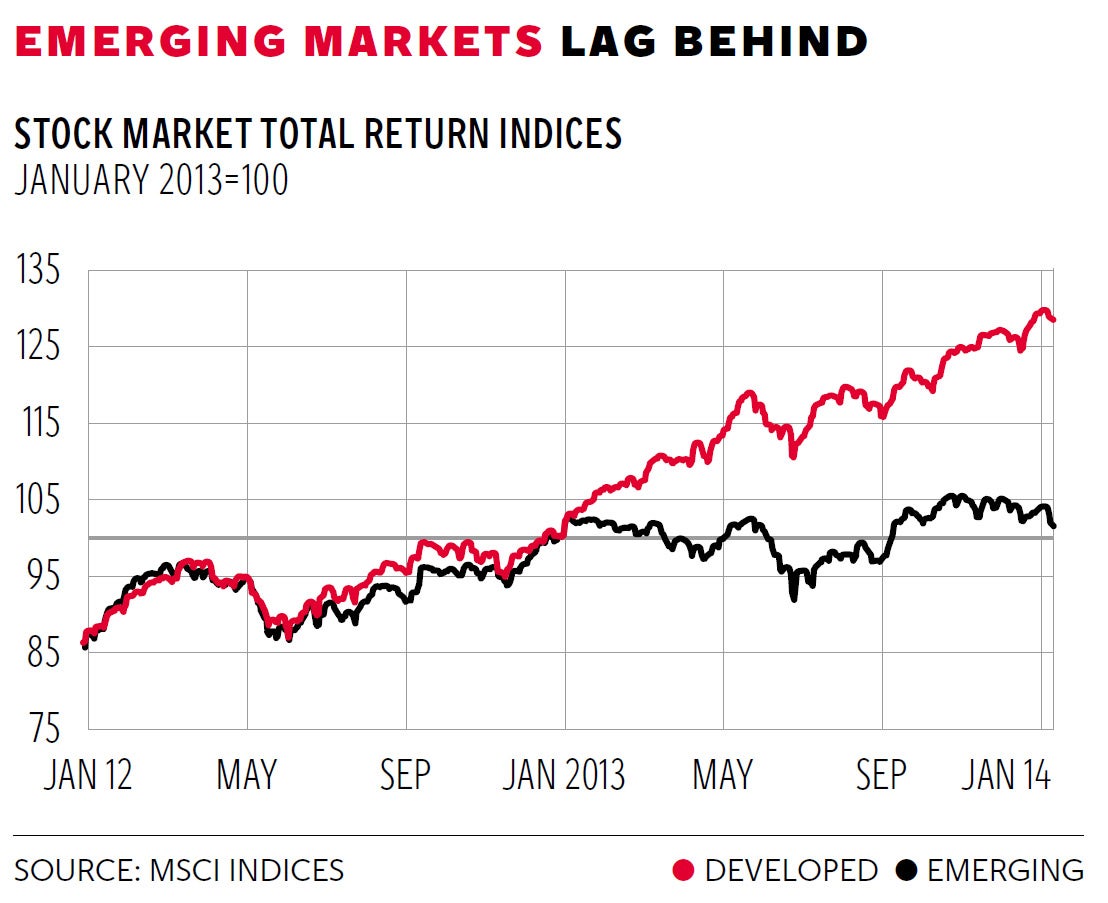

Except that it didn't turn out like that. If you take as your benchmark the performance of equities, last year was a bit of a disaster for this strategy. As you can see from the graph, 2013 was the year when emerging markets moved sideways while developed markets shot ahead. Is the great emerging market run over?

Some of its previous enthusiasts think so. For example, last month Goldman Sachs's investment management division told clients to cut their emerging market exposure by one-third, from 9 to 6 per cent of their total portfolios. It was Jim O'Neill, until recently head of the investment side of Goldman, who coined the Bric acronym for Brazil, Russia, India and China, and has now come up with the idea of the Mints (Mexico, Indonesia, Nigeria and Turkey) which he is promoting on BBC radio. Since he left, Goldman has rather shifted its stance. It now predicts "significant underperformance" over the next 10 years.

Others broadly agree. Morgan Stanley thinks that three key emerging market currencies will fall this year by up to 17 per cent – the Russian rouble, the Brazilian real, and the Turkish lira – and will suffer more generally when the Fed tightens monetary policy. Deutsche Bank projects that emerging market returns will be 10 per cent lower than developed ones this year. JP Morgan Chase notes that political uncertainty in several important emerging markets is rising, and that Brazil, Turkey and India all face elections this year. Citigroup put out a paper highlighting rising debt levels in emerging markets, making it hard to maintain the improvement in credit ratings that has been running for several years. And so on.

What should we make of all this? I think there are several forces at work. One is simply fashion. After the extraordinary attention paid to the emerging world over the past five years there was bound to be some sort of reaction and we are seeing that now. Commentators tended to be inspired by the growth and to pay less attention to the imbalances associated with that growth.

Another is that the developed world, southern Europe apart, is performing rather better than it was and is producing good returns for investors. There is still a huge gap between the expected growth in the developed world, an average of about 2 per cent this year, and that of the emerging world, about 4.5 per cent. But the gap is not nearly as big as two or three years ago.

Finally, you have to make a distinction between growth and the performance of investments. The main source of net savings in the world is the flow from the emerging economies, especially China of course, but also other big ones including Russia and India. The choice of investors has often been to shift funds to the developed world – we see that in all sorts of ways – so the locals are getting their money out. They probably have good reasons for doing so that the rest of us should listen to.

My own reaction to all this is to note that emerging economies are, well, emerging. They will for the foreseeable future continue to outpace developed ones. But the extreme conditions of the past four years are now drawing to a close and we can start to look at both classes of economy – and their investment opportunities – with a more measured eye.

We have a growth disadvantage in the developed world but we have a governance advantage. Not only do we have less capricious governments; we also have in the main less nationalistic ones in the sense that regulation and taxation will not discriminate against foreign investors. The few developed countries that in one way or another do favour local investors don't attract much foreign funding. Weak governance, or at least weaker governance, requires higher returns to compensate for the risk.We also have an inflation advantage. Average inflation in the developed world is about 2 per cent; in the emerging world it is 5 per cent. You can compensate for this by focusing on real returns rather than money ones but higher inflation is generally more volatile inflation, another risk factor.

Historically this has led to higher overall returns in the emerging world. The issue is how much higher returns are needed to compensate for those higher risks. Historically too, investors have not been good at assessing emerging market risk, though to be fair, they have not been too cute at assessing developed market risk either, as the swings in the fringe European bond markets over the past couple of years have demonstrated. On a long view there can be little doubt that emerging markets will, taken as a group, become more like developed ones. The GDP per head gap will narrow; the middle class will expand; financial governance will improve. We should not assume that the Western model of investment will be adopted in its entirety, nor would that be desirable. There are plenty of flaws in the way we do things. But on a long view it would be reasonable to expect higher investment returns in the emerging world than in the developed world.

On a shorter time horizon, say three years, this may not be the case. The cyclical recovery of the developed world has some way to run, or at least if it doesn't and we have another recession in a couple of years' time we are all in trouble. Assuming then that the present growth phase widens and deepens, and assuming returns in the developed world remain decent, investors will not be under such pressure to look elsewhere.

This does not however mean the shift of economic power to the Brics will ease much. Steadily, year by year, power will continue to move. It is just that this will be a less dramatic shift than it was, say, three years ago.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments