David Blanchflower: Why isn't the Bank more transparent?

Economic Outlook: A big concern is that the Bank provides little detail of its forecasts, and no information at all on its new Compass model

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.It was always going to come to this. The Monetary Policy Committee threw up its hands last Wednesday and gave up the charade that all was going to be well by 2015. It finally had to admit its growth forecasts have been overly optimistic for years and is forecasting the UK economy is heading back into triple-dip recession. To quote from the Inflation Report: "In Q3, output increased by 1 per cent. In Q4, that growth rate seems set to fall sharply as the boost from the Olympics is reversed; indeed, output may post a small decline".

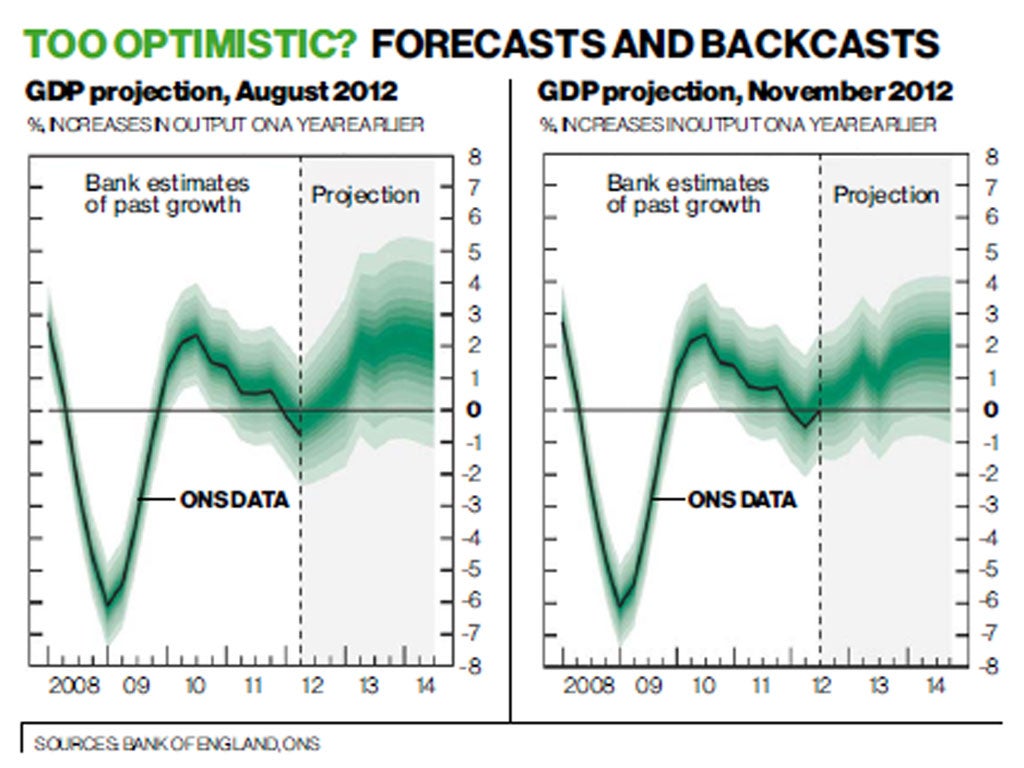

The growth forecast was considerably less optimistic than the one produced in August, which I criticised at the time for being from Cloud Cuckoo Land. And so it has turned out. The chart on the right above shows their latest forecast for growth in the form of their now infamous GDP growth fan chart, which is conditioned on Bank Rate remaining at 0.5 per cent and with £375bn of asset purchases. This shows that the MPC expects growth, shown by the dark swathe in the centre of the fan on the right, of only 2 per cent in 2015 compared with their earlier forecasts of 3 per cent and more. The MPC is forecasting that the drop in output of 6.3 per cent that occurred from 2008Q2 through 2009Q2 will not now be restored before mid-2014, six years after the recession started. In contrast, the drop in output in the 1930s, which was around 8 per cent, was restored in four years.

The so-called "backcast" to the left of the horizontal line shows the official ONS data. And the fact that the green fan lies close to that line means the MPC doesn't share the views of the "recession deniers" that the latest downturn was a statistical chimera that will eventually be revised away. Such claims, of course, were never credible given that, over the last 10 years, the average quarterly revision by the ONS has been zero.

It is clear from Sir Mervyn King's comments at the press conference that most of the changes to the outlook come from a change in the committee's judgements about the chances of very positive outcomes. Some decline in growth of course comes from the rise in inflation, which acts to depress real wages and hence consumption. One of the major differences, though, compared with the August forecast is that in the new forecast the fan only goes up to 4 per cent, whereas in the previous one it went close to 6 per cent, which I criticised at the time as highly unlikely. In both forecasts the fan stops below at around minus 1 per cent. To quote Sir Mervyn directly from the press conference: "The chances of a rapid recovery are a good deal less than we thought. So in our previous fan charts we did have some probability attached to pretty rapid recovery growth rates of 4 per cent or more. I think we feel that the persistence of the weakness in the world environment has been such now that we attach much less weight to those very rapid growth outcomes; though we don't attach any greater weight to much weaker out-turns". The forecast does certainly look more plausible now. A worry is that it still may be too optimistic.

A big concern is that the Bank provides little detail of its forecasts, and no information at all on the new model it has started using, called Compass. David Stockton in his recent review of the Bank's forecasting performance pointed out: "Compass has now been in active use by the staff as input into the forecast for nearly a year. However, interested parties outside the Bank have little to no understanding of the model and its key features." The Oxford economics professor Simon Wren-Lewis on his Mainly Macro blog* observed that "when monetary and fiscal policy was in the hands of the UK Treasury, the Treasury model was subject to detailed scrutiny". He goes on to conclude that "it does seem regrettable that the Bank has been using a model to produce its forecast for a whole year that no one knows anything about".

An official Bank spokesperson told me: "Spencer Dale set out the Bank's modelling philosophy in a speech in March, and since then Bank staff have given presentations on the new model to colleagues at other central banks and to the IMF. We intend to publish a working paper setting out the model in detail, and give a programme of presentations at UK universities in the new year."

As Fed Governor Janet Yellen made clear this week in an important speech "a growing body of research and experience demonstrates that clear communication is itself a vital tool for increasing the efficacy and reliability of monetary policy". Bank of England take note; the time to be transparent is now.

On the same day as the MPC forecast, the ONS released the labour market data which showed the biggest rise in the claimant count for a year of 10,000 between September and October. The next day we had horrid retail sales numbers. That led David Kern, chief economist at the British Chambers of Commerce, to argue that "GDP will see a sharp slowdown in the fourth quarter".

So despite George Osborne's claim that the economy is healing, we are likely to see three quarters of negative growth, with one Olympics-driven quarter of positive growth followed by another negative one. Indeed, the economy shrank by 0.1 per cent over the last 12 months. Four out of five quarters of negative growth would stand in marked contrast to the US, which has had 13 quarters of positive growth in a row. To rub salt in the wound the credit rating agency Moody's suggested that if this happens the UK would likely lose its AAA credit rating. This represents a major problem for Mr Osborne, who seems to have believed that all would be well in 2015. That dream looks to be in tatters. I am looking forward to the Autumn Statement with much interest.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments