David Blanchflower: The OBR's credibility is in tatters

Chancellor is fiddling at the edges as the economy flatlines

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.It wasn't exactly an auspicious start to Budget Day. Three pieces of evidence were published this morning, a few hours before the Chancellor stood up to speak, that shed light on how the austerity plans are working. They aren't. Cutting public spending and culling public sector jobs was supposed to lead to a resurgence of the private sector, it hasn't and was never going to.

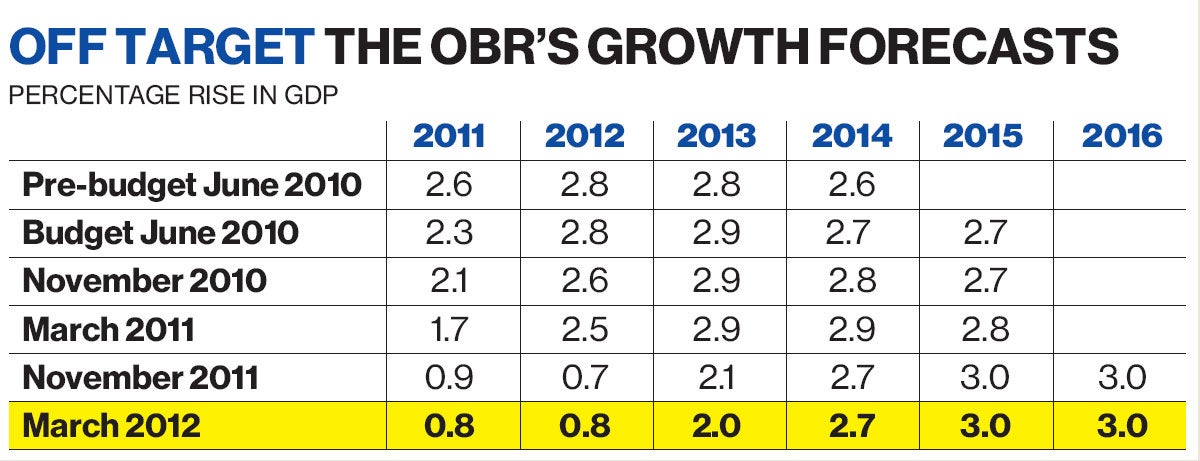

Click HERE to view 'Off target: The OBR's growth forecasts' graphic

What we heard from our part-time Chancellor in the afternoon in this fiscally neutral Budget, was more of the same, which will inevitably produce more of the same; little or no growth and rising unemployment especially among the young.

First, the public sector net borrowing hit a record for the month of February, rising to £15.18 billion, which was twice what economists had expected. The lack of growth has meant that tax receipts are down 2.7% on a year ago, principally from declining income tax receipts. Government spending is up by 8.3% on a year ago, because of higher social benefits due to rising unemployment and government departments turning on the taps.

On top of that the Chancellor has claimed that a measure of the success of his policies has been the decline in the government's costs of borrowing. Following that reasoning, the fact that UK ten-year gilt yields have increased rapidly from 2% at the end of February to close to 2.4% during the month of March should be seen as an indictment of Osborne's policies by the markets. He can't have it both ways.

Second, the minutes of the February MPC meeting showed that two members, David Miles and Adam Posen dissented from the majority view and voted for an additional £25 billion of monetary stimulus because of "the risk that persistently weak growth would damage the future supply capacity of the economy". Even the majority argued that there were significant risks to the downside. The MPC's growth forecast produced in the February 2012 Inflation Report still looks wildly optimistic, and as with all of the last fourteen forecasts they have produced, will also be revised downwards.

Third, the Bank of England's Agents reported on the state of the economy. Their scores provide a useful indicator on where the economy is going and gave an early indicator of the recession to come in early 2008. Their report is consistent with the February PMIs, which suggest continued slowing of the economy. Employment intentions in the private sector remain flat. Credit conditions had tightened as a result of which the demand for loans remained fairly weak. Most worryingly investment intentions were broadly flat.

If we look back at the OBR's pre-Budget forecast in June 2010 growth in the UK was supposed to be driven by business investment, which was predicted to grow by 8% in 2011, 9.8% in 2012 and in double digits after that. It turns out that in 2011 it grew by 0.2% and in the new forecast the OBR expects investment to in 2012 to grow by only 0.7%. But no worries, the OBR's forecast is for investment then to take off, growing by an unlikely 6.4% in 2013; 8.9% in 2014 before hitting double digits in 2015 and onwards. Pigs might fly.

It is unclear what the game changer is supposed to be that will boost business investment over the next two years when it hasn't done so over the last two. Just like the MPC, the OBR's forecasts have been wildly optimistic and have had to be revised down as the economy tanked. For example, the OBR's initial forecast for 2012 was 2.8% compared with 0.8% today. The odds are that today's forecasts will be downgraded, given that the vast majority of spending cuts have yet to hit and there are continuing risks from the Euro area and high oil prices. This really is 'fingers crossed' economics from an OBR whose credibility is in tatters.

This is a Budget that fiddled at the edges as the British economy flatlines. It remains unclear where growth is supposed to come from; more of the same simply doesn't do it. Osborne still has no growth plan.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments