David Blanchflower: Heard that the UK's the fastest-growing economy? Don't you believe it

Evidence that the economy began to slow in late spring was apparent in the Bank of England agents’ report

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

Your support makes all the difference.In an opinion article on 14 December in The Wall Street Journal the Chancellor, George Osborne, claimed that “the UK has been growing faster than any other major advanced economy”. This is pretty careful wording because he didn’t say the UK currently is growing faster than any other advanced country. Why? Because the UK isn’t growing fastest.

It seems like a good idea to take a quick look at the data for the last five quarters in order. First the UK: 0.8 per cent, 0.5 per cent, 0.8 per cent, 0.9 per cent, 0.8 per cent. And then the United States: 1.1 per cent, 0.9 per cent, -0.5 per cent, 1.1 per cent, 1.0 per cent. The US has had faster growth in four of the last five quarters. It has had three quarters in the last five with growth rates of 1 per cent or higher, compared with none in the UK. The US grew faster over the last two quarters and in the most recent quarter it also grew faster than the UK (1 per cent and 0.8 per cent respectively).

Any claim about the UK’s superior performance rests entirely on the bad weather, broken ankle, now long gone, first quarter in the US of 2014. Most forecasters predict that the US will also grow faster than the UK in 2015 and 2016.

Last week on the markets was action-packed. Oil prices have halved since the summer. My son paid under $2 a gallon for gas in Texas over the weekend. Commodity prices have also plunged. The Bloomberg Commodity Index is down by a fifth since the summer. The rouble has halved in value in a few months. In the middle of the night the Russian central bank raised rates from 10.5 per cent to 17 per cent. Moscovites rushed to stores to buy consumer durables before their prices rose. The concern for the Russians is as they don’t export much other than oil and gas and the fall in the exchange rate will have little domestic benefits.

There are no signs that there is about to be a burst of tourists arriving to take advantage of the cheap prices. They are likely headed to Cuba, where prices really are low!

Elsewhere the Swiss central bank moved to negative interest rates. The equity markets around the world went into a tizzy on concerns that this was being driven by a fall in demand, especially in China, alongside concerns about defaults on Russian debt, although they picked up subsequently. There was little sign of demand picking up in response to the falling oil price. The hope is cheaper oil will boost world growth.

On 5 January 2014, in this column, I admitted that the big mistake I made in 2013 was not seeing a European-wide improvement in business and consumer sentiment coming. I said then: “I should have realised that this positive burst in sentiment predicted a burst of both growth and employment. My error.”

I don’t want to make another unforced error. What has now happened is that these same surveys all turned down together around the spring of 2014 in the eurozone, the UK and many EU countries, including Germany. The EU’s Economic Sentiment Index, which is a composite of four business surveys in retail, construction, production and services and also a consumer survey, is down from spring peaks in both the EU28 and Eurozone 18, as well as in the UK.

All five of these surveys for the UK have slowed since the spring. Markit’s flash composite PMI for Germany showed private-sector output growth slowing to an 18-month low. The concern is that this is indicative of a European-wide slowdown in growth, the exact reverse of 2013.

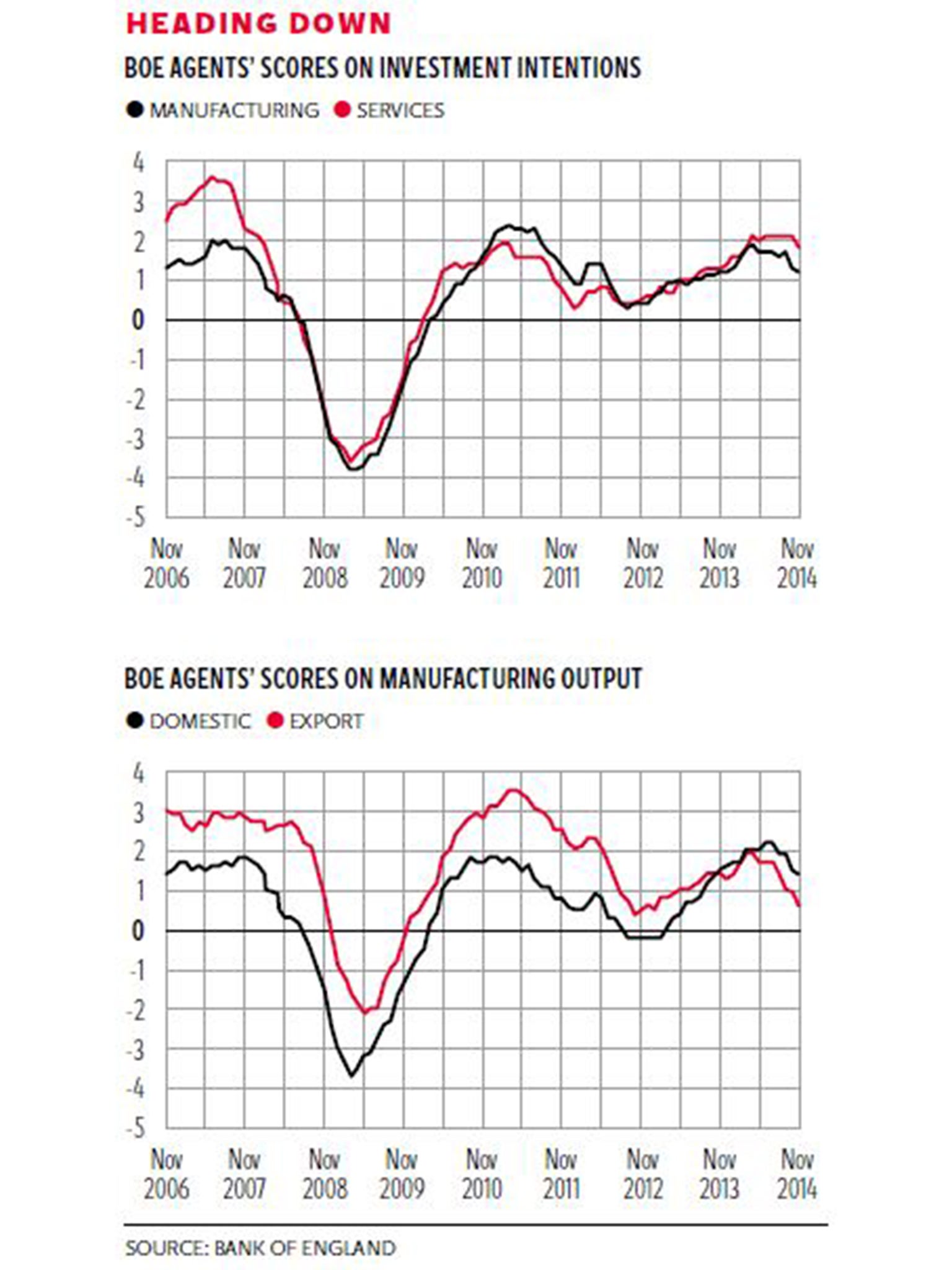

Evidence that the UK economy began to slow in late spring was especially apparent in the December report of the Bank of England’s agents. The 12 agents, with offices in each of the UK regions, are the eyes and ears of the MPC, talking to businesses around the country and assessing changes in economic conditions. In their report the word “ease” appeared 23 times. For example, they found that retail sales values growth had eased, housing market activity had continued to slow and house price inflation had softened. Employment intentions had eased slightly for manufacturers. Investment intentions for the next 12 months had eased slightly. Manufacturing output growth for the domestic market had eased, and manufacturing export growth had slowed.

The agents take the market intelligence they have received as an ordinal rather than cardinal score, where a higher number is better. The first chart plots the scores for investment intentions in manufacturing and services. Of particular note is that the collapse in these scores predicted the oncoming Great Recession – they fell sharply from 2007. There is a marked uptick that I missed in 2013, but that ceased in the spring of 2014 and has turned down, more markedly admittedly in manufacturing than services.

The second chart plots the agents’ scores for manufacturing, separated out by domestic and exports. These scores also plunged in 2007, predicting the Great Recession that was to come. The pick-up in 2013 is notable, but the concern is the marked decline in both since the spring of this year, matching the decline in investment intentions. Employment intentions have a similar downward path from spring 2014.

Elsewhere, claims of a real wage pick-up are unfounded. The latest data we have says that nominal wage growth continues to fall for the 36 per cent of workers who are self-employed or work in firms of less than 20 employees. Total pay in the upward-biased Average Weekly Earnings (which excludes such workers) was up 1.4 per cent in October, compared with a 1.3 per cent rise in the Consumer Price Index in October. The 1 per cent inflation figure reported last week is for November. Real earnings are down 0.7 per cent if the Retail Price Index is used.

This is only the second month in 54 that AWE growth was higher than the CPI since the Coalition took office. There has never been a positive real month if the RPI, which is the most widely used inflation measure used for wage settlements, is used.

The ONS experimental whole economy Index of Labour Costs per Hour (ILCH) series was published last week and increased by 1.3 per cent in the third quarter of 2014 compared with the same quarter of 2013, which is also consistent with real wage falls. Real wages continue to drop.

And this decline in sentiment likely predicts a slowing of the UK economy. I am on top of it this time.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments