David Blanchflower: Beware - the American jobs market is still feeling the chill

There was a surge in hidden unemployment in the wake of the Great Recession

Over the past year, the US economy has added more than 3 million full-time jobs. While this is undoubtedly good news for American households, the economic recovery remains far from complete. Indeed, the proportion of adults in their prime working years who have jobs is still markedly lower than at the start of the Great Recession; the number of people working part-time who are unable to find a full-time job remains elevated; and a host of nominal wage indicators show no signs of any incipient inflation pressure.

Consequently, in light of our own empirical research, we broadly share the latest economic assessment of the Congressional Budget Office (a non-partisan agency that provides independent analysis to the US Congress), namely, that, just like in the UK, labour market slack remains substantial and will only diminish gradually over the next couple of years. Moreover, we see clear downside risks to the outlook for economic activity and inflation.

These considerations are crucial for informing the monetary policy decisions of the Federal Open Market Committee (FOMC), which has a legal mandate to foster maximum employment and price stability. About two months ago, the FOMC stated that it would be “patient” in determining the appropriate time to initiate monetary policy tightening. Since then, however, some Fed officials have begun suggesting that such patience is no longer needed and that monetary tightening should commence later this spring.

We believe that such a policy move would be a grave mistake. In particular, our analysis underscores the following reasons why the Fed should remain patient.

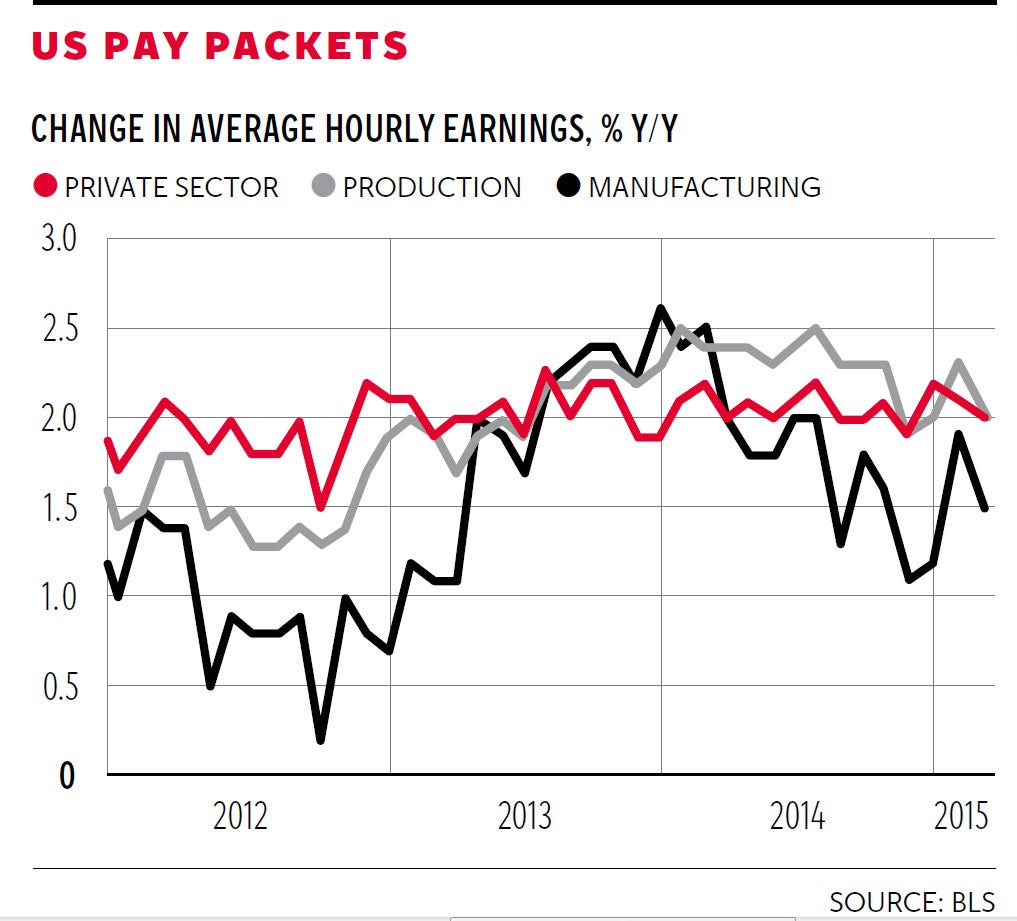

First, nominal wages. Labour compensation decelerated markedly in the wake of the Great Recession, and since then nominal wage growth has remained mired at around 2 per cent. In effect, real wages (that is, adjusted for consumer inflation) have remained essentially flat. As shown in the chart, that trend remains evident in the latest earnings data released last week by the Bureau of Labour Statistics (BLS).

Of course, these series often exhibit transitory month-to-month fluctuations that reflect sampling variability and other special factors. For example, average hourly earnings for all private non-farm employees dropped from $24.68 last November to $24.63 in December and then picked up to $24.75 in January, but the annualised two-month change was only 1.7 per cent.

Furthermore, that measure of earnings can be strongly influenced by movements in the upper tail of the wage distribution, and hence it may be less informative about broader wage trends. In fact, the latest BLS release indicates that the average hourly earnings of non-supervisory and production workers (who comprise the bulk of the American workforce) increased from $20.77 in November to $20.80 in January – a measly 3 cent raise that corresponds to an annualised growth rate of just 0.8 per cent. Earnings in manufacturing are currently growing at 1.2 per cent, down from 2.0 per cent last summer. In effect, once we smooth through the monthly noise, the recent data on nominal wage growth is fully consistent with the assessment that labour market slack remains substantial.

Second, hidden unemployment. The conventional measure of unemployment only includes those who are actively looking for work. Consequently, we use the term “hidden unemployment” to refer to those adults who have given up searching for work but would return to the labour force if the job market was sufficiently strong.

In past decades, the conventional measure of unemployment was generally viewed as a sufficient statistic for summarising the extent of labour market slack, but in recent years that has simply not been the case. In the wake of the Great Recession, millions of Americans gave up searching for jobs. For example, among adults aged 25 to 54, the labour force participation rate is currently 2 percentage points lower than it was at the end of 2007.

Fortunately, the latest BLS report confirms that the post-recession surge in hidden unemployment should not be viewed as irreversible. Last month, more than 500,000 people rejoined the labour force. In fact, the labour force expanded even faster than the level of employment, and hence the unemployment rate moved up a notch – hardly a sign of labour market tightening. Moreover, our research provides compelling evidence that hidden unemployment in the US places significant downward pressure on wages, because employers often fill job vacancies by hiring people who have just rejoined the labour force and hence were never counted among the unemployed.

Of interest is the fact that participation rates in the UK rose steadily throughout the Great Recession but have gone into reverse in the last few months or so. This means that in part the recent fall in unemployment is because people have left the labour force.

Third, under-employment. Although the labour market has been steadily improving, many Americans remain under-employed, that is, they are willing and able to work full-time but are only working part-time due to slack demand or because they cannot find a full-time job. Our analysis indicates that at least one million more full-time jobs are needed to bring the incidence of under-employment back to the levels that prevailed prior to the Great Recession.

Furthermore, it is evident that this form of labour market slack places downward pressure on wages, because employers may well fill a full-time position by hiring an individual who had previously been working part-time (either at the same firm or elsewhere).

Finally, employment. We estimate that 4 million full-time jobs must be created in order to close the US employment shortfall over the next two years. In particular, labour market slack – including under-employment and hidden unemployment as well as conventional unemployment – is currently equivalent to 2.7 million full-time jobs. In addition, demographic factors imply an upward trend in the labour force of 50-60,000 per month. Thus, if non-farm payrolls continue to rise steadily at a monthly pace of about 200-250,000 jobs (that is, roughly the same pace as in recent quarters), then our analysis indicates that the employment gap would not be eliminated until 2017. In effect, a reasonable benchmark for the US economy is that two more years will be needed to get to full employment.

This article is jointly written with Andrew Levin, who spent two decades at the Federal Reserve, most recently as a special adviser to the Board from 2010-2012. He will be joining the economics faculty at Dartmouth College this summer.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks