How to navigate the mortgage market when rates are rising

THE ARTICLES ON THESE PAGES ARE PRODUCED BY BUSINESS REPORTER, WHICH TAKES SOLE RESPONSIBILITY FOR THE CONTENTS

Rose Capital Partners is a Business Reporter client

With interest rates looking set to rise, what does it mean for the mortgage market?

Recent events in both financial markets and the wider economy mean that interest rates look set to rise sooner than expected.

A fall in unemployment from 4.6 per cent of the working population in August to 4.5 per cent in September – according to official Office for National Statistics (ONS) data – would not normally be noteworthy. We saw the furlough scheme come to an end in September and the Bank of England had concerns we would see a spike in unemployment, but that has not materialised. The ONS also expects wage inflation to continue. Wages were up 7.2 per cent in Q3 2021 vs Q3 2020 and predicted to rise between 4.1 per cent and 5.6 per cent in Q4 2021 vs Q4 2020.

Inflation doesn’t look to be going away anytime soon. Even with a surprise downturn to 3.1 per cent in September vs 3.2 per cent in August, it is still more than 50 per cent above the target level of 2 per cent set by the Bank of England. In October, we saw real issues around fuel supply, energy prices and supply chain issues, so inflation may well hit 5 per cent before it starts to peg back. Andrew Bailey, Governor of the Bank of England, was quoted as saying it “will have to act” over rising inflation, which was a very clear reference it intends to raise the base rate up from its current level of 0.1 per cent.

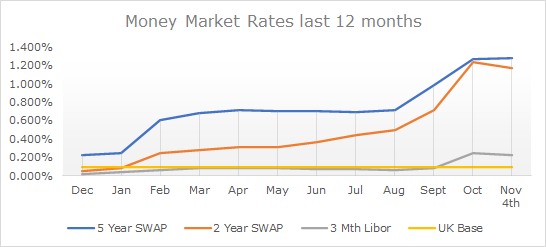

Money markets had already started to shift in September as much of this data started to filter through.

As the vast majority of mortgage lenders buy in their funds from money markets, it is a strong indication of where mortgage rates will go as they often have to act ahead of any movement from the Bank of England. The above picture tells us that we can expect around two base rate rises over the next two years, closing out 2022 at around 0.5 per cent, but only one more is likely after that point to 2026. So while interest rates are set to rise, they do not look like they will go up sharply or much higher than where we are now. The sheer level of debt in public and private finances means it will be a ‘steady as you go’ approach from the Bank of England.

Inflation and the mortgage market

The obvious answer to all this is to look for a longer-term fixed-rate product, but this comes with a number of risk warnings and caveats to achieve the best outcome.

As a rule, if you have more than a 25 per cent deposit when you look to arrange a mortgage, you are likely to get a rate of less than 1 per cent. These are likely to be the lowest that mortgage rates will ever be, so fixing in for five years makes a lot of sense. If you have less than 25 per cent equity, it may well prove cheaper to take a short-term deal now and fix for the longer term afterwards.

Mortgages become much cheaper when you have a magical 25 per cent equity as house prices have never fallen by more than 25 per cent in any one cycle, so banks deem you as low risk – hence the preferential pricing.

If you are looking at moving, or perhaps had a credit blip in the recent past, fixing for the longer term may not be for you. As per the above, it may make sense to go shorter term, or even take a penalty-free product so you can move or renegotiate the product once the event has passed that is stopping you from getting the lowest priced products now.

It’s not recommended that you fix for more than five years, as products past that term become disproportionately expensive. There are two reasons why: firstly, the cost of funds are far greater, as no one can predict the future, and secondly, the risk of you defaulting goes up over time, so banks also need to price in that risk on top of the usual product pricing.

Once you have a clearer idea of what path to go down, finding the most suitable product and lender becomes much easier. Everyone’s situation is unique, so there is never a one-size-fits-all approach and it is strongly encouraged that you get specific financial advice before going ahead.

If you would like personalised advice, contact one of the team at Rose Capital Partners to discuss what all this means and the best course of action for you.

Originally published on Business Reporter

Bookmark popover

Removed from bookmarks