Hamish McRae: Money is cowardly – that’s why we have seen it running away from Scotland this week

The less-clear message is that holders of Scottish assets are wary of independence

The events of the past week in Scotland have demonstrated one thing clearly, and one less so. The first is that investors everywhere in the world hate uncertainty. The sharp fall in sterling is testimony to that. The less-clear message is that holders of assets in Scotland itself are wary of independence. There has been an outflow of liquid funds, as yet unquantified but evidently considerable, into banks south of the border.

The first is rational enough. There have been a string of reports suggesting that the pound would decline by about 10 per cent in the event of a “Yes” vote next week, and whether these concerns are reasonable or not, why take the risk? The second is less so. There is no question of an immediate currency split. The Royal Bank of Scotland is 81 per cent owned by the British government. And Lloyd’s Bank, while technically headquartered in Edinburgh following its disastrous takeover of Halifax Bank of Scotland, would return to London in a flash. There is really no immediate reason for concern, whatever the outcome, though there is an obvious danger of currency flight in the medium term.

Click graphic above to enlarge

Beyond these two observations what can – from an economic perspective – sensibly be said about the events of the past few days? There is no point in retracing the arguments as to the advantages and disadvantages of independence, which have been kicked around for the past couple of years. What is interesting is what we have learnt. Here are five propositions:

The first is that whatever the outcome both of the referendum and the subsequent changes to the fiscal arrangements for Scotland – massive in the case of a “Yes” but still considerable in the case of a “No” – the basic structure of both economies remains the same. Things do not change overnight. Companies do not suddenly collapse, for the goods and services they produce are still needed. Depending on the outcome there may be some negative impact on both consumer and investment confidence. But confidence reacts to reality and if the real economy, or maybe economies, carry on growing then confidence will recover too.

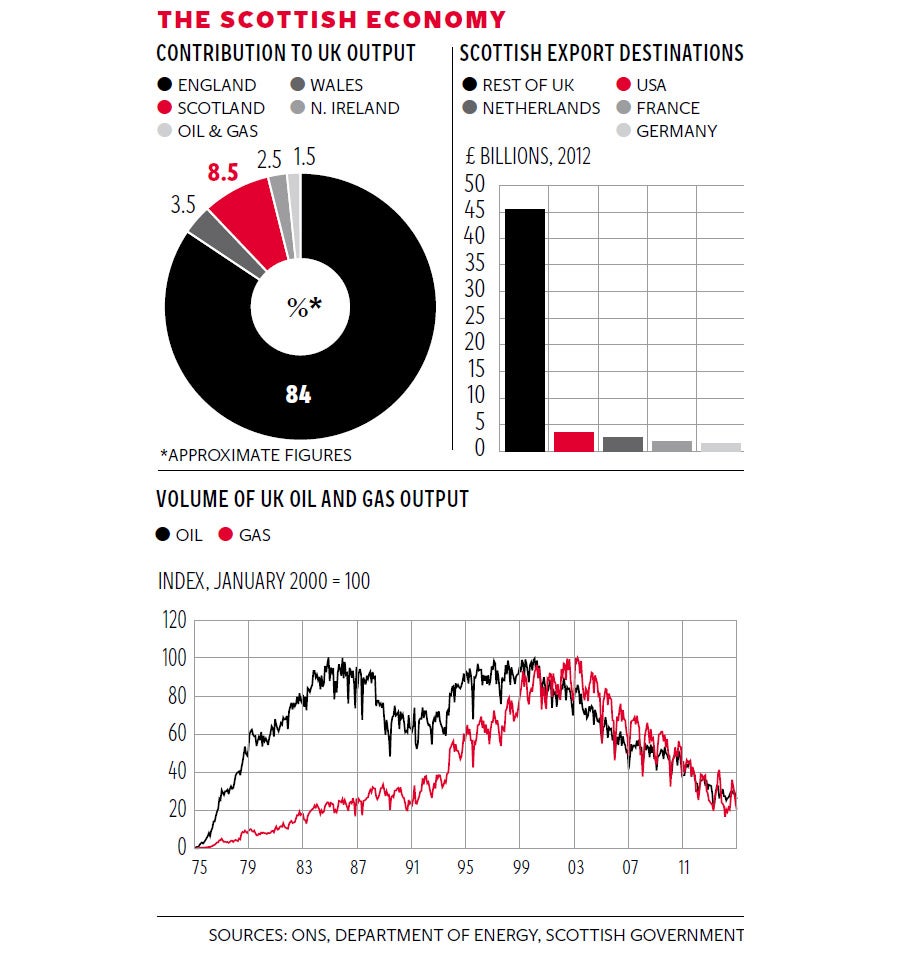

As you can see from the pie chart, Scotland is roughly 8 per cent of the UK economy, but that is three years’ good growth. It would take longer for the remainder of the UK to replace Scotland’s population, about 10 years, but growth is the thing that matters.

The second is the significance of the sterling issue. Had the euro been a huge success this would not matter. Currency unions without political union would appear to be workable and in the event of independence Scotland would have a choice of which to join (the early plan was for euro membership). But the euro has been at best a difficult union to manage and at worst an economic and human catastrophe.

So people have to factor in the possibility of an independent Scotland operating an independent pound, as Ireland did in 1979. But – and this is the key point – there is nothing wrong with that. The Irish government in 1979 argued that it needed greater currency flexibility and the ability to set its own interest rates. The Irish economy experienced some pretty big bumps but overall it performed as well during the period it had an independent currency as it had done with a link with sterling. As far as Scotland is concerned, some £47bn of its exports go to the rest of the UK (see bar chart), so it remains extremely important. But £12bn go to the EU, and £13bn to the rest of the world, with these markets rising faster than the UK. All these figures exclude oil and gas exports, which, while in long-term decline, do remain considerable, as the bottom graph shows.

The third proposition is that the status quo on fiscal policy is not sustainable. We have learnt that in the past few days, with the proposition of a substantial redrawing of the fiscal relationship with the rest of the UK in the event of independence being rejected. In the short-term there will be the negative consequence in that uncertainty over fiscal policy increases whatever the result of the referendum. But in the long run there is a positive prospect of greater tax competition between Scotland and elsewhere in these islands. We are going to see both Westminster and Edinburgh trying harder to craft tax policy to boost economic activity as well as gathering revenues in the most-effective and least-damaging way.

Proposition four is that irrespective of the outcome, much more attention will be paid by London to the rest of England. Power will devolve to the regions; the UK will become a less-centralised state. You have to be very pessimistic about the quality of local decision-making not to expect better outcomes for what are at present the less-prosperous parts of England. This is surely an unequivocal plus, resulting in a more-balanced country as well as one that is likely to become more successful in economic terms.

Finally, if that will be a long-term advantage to England – particularly the north – there are potential, long-term costs to Scotland, whatever the outcome. The model here is Canada, where the possibility of separation has been a drag on the Quebec economy since the 1960s. The first referendum on independence in 1980 was comfortably defeated, but the second, in 1995, was within half a percentage point. Well in advance of all this business had already been shifting to Ontario and the movement speeded up from the 1980s onwards. So there will need to be reassurance from the Scottish government towards the business community and that will have to be convincing. Even so, a gradual shift of business is probably inevitable.

Ultimately this is about politics, not economics. But politics do shape economics and this transfer of money out of Scotland, however irrational that might be, must at the margin have some political impact. It is unpleasant to have to acknowledge this but money is cowardly, as we have seen this week.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments

Bookmark popover

Removed from bookmarks