What can investors learn from previous hung parliaments?

Here’s what history tells us about the financial effects of hung parliaments and coalitions

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

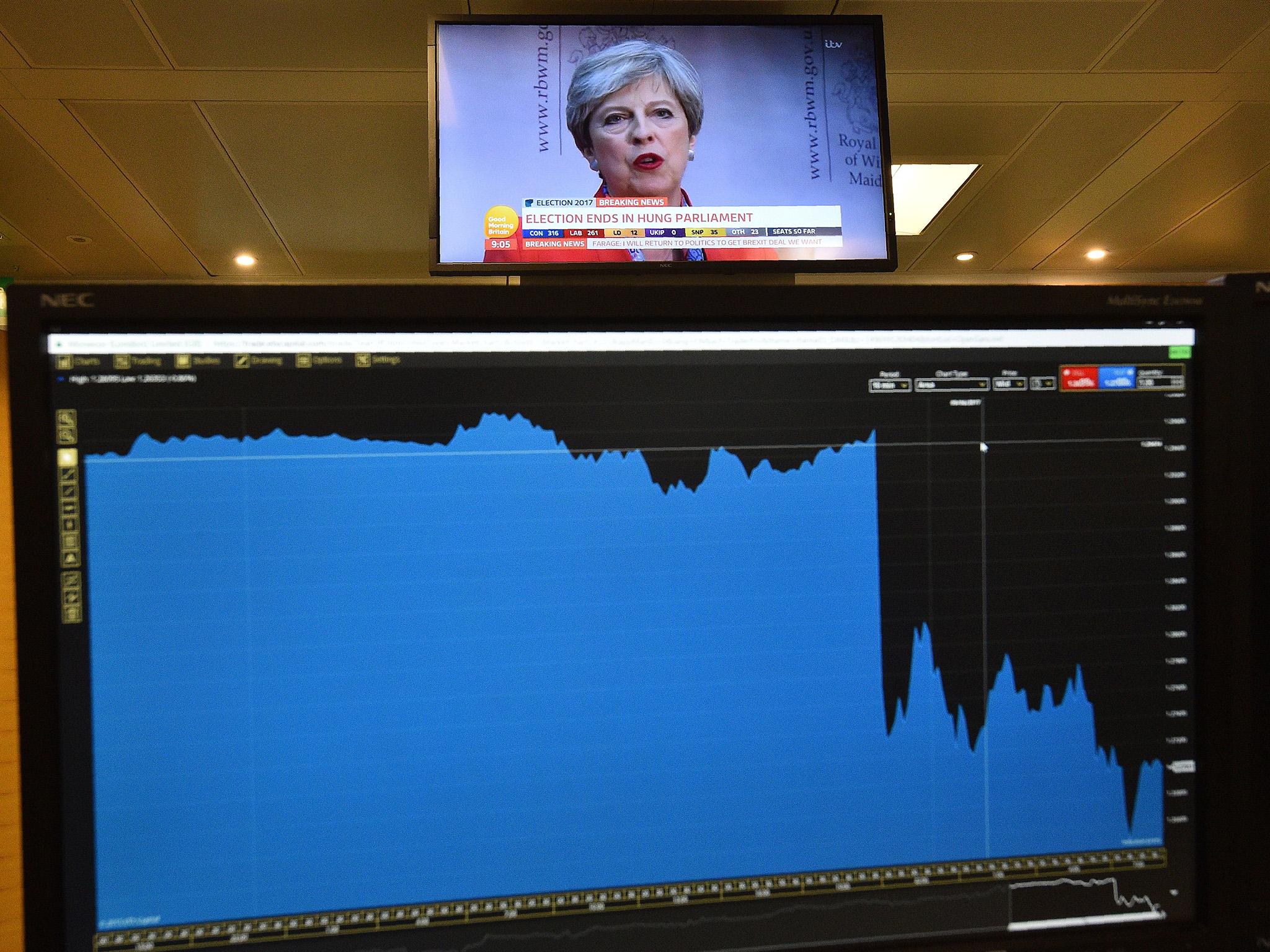

Your support makes all the difference.Whether you call it a coalition of chaos or a stable new partnership, the current situation in Parliament has caused ripples for everyone’s finances.

Immediate implications included a sharp fall in the pound, while both the benchmark FTSE 100 and the FTSE 250 have risen since the surprise result was announced.

The news that inflation has hit new highs too, while income has been squeezed, suggests that lower consumer spending will have a further weakening impact on the economy, especially on those companies that rely heavily on domestic markets.

Pundits have been quick to predict a bumpy road ahead for those of us with investments. The stock market does not like uncertainty, and as one fund manager, Ketan Patel from EdenTree, put it: “The absence of a ‘strong and stable’ government presents a complex investing landscape, with more plot twists to unravel over the coming days and weeks.”

With little certainty to cling on to, turning to history is one of the few ways to try to unravel investment strategy for the coming months or years. Looking at Britain’s most recent hung parliaments, the events of 2010 and 1974, and even 1929 offer wildly different suggestions of how the markets might react.

2010 – The Conservative-Liberal Democrat coalition

The election result in 2010 saw a 2.6 per cent fall in the FTSE on the day of the results, but recovery was quick after early wobbles. Incumbent prime minister Gordon Brown resigned, and the markets began to recover. By the time the Conservative-Liberal Democrat coalition was announced, the benchmark FTSE 100 had gained 2.3 per cent compared with the day before the ballot.

While sterling fell immediately, the losses came to barely 0.5 percentage points against both the euro and the dollar by the time David Cameron and Nick Clegg had formed their coalition. Prices for gilts fell slightly.

“The scope for short-term swings is clear – but note that markets calmed down pretty quickly as economic and company fundamentals reasserted themselves,” says investment director Russ Moulds of AJ Bell.

Over the 12 months following the 2010 election, the FTSE rose 13.6 per cent while the 10-year gilt yield fell (so price rose) from 3.74 per cent to 3.40 per cent. The pound gained 10 per cent on the dollar and lost 4 per cent against the euro in the 12 months after the poll.

1974 – A year of two elections

Many people are drawing parallels with the snap election of 1974, when Tory prime minister Edward Heath lost 37 seats and was overtaken by Harold Wilson’s Labour Party.

Heath’s efforts to forge a coalition with Northern Irish Unionist MPs and Liberals failed, and Heath quit a week after the election.

While Theresa May must hope that history won’t repeat itself, investors might think the same thing. The 1974 election caused a 6.4 per cent fall in the FTSE All Share the day after the ballot, and the fall just got worse and worse and worse. The All Share finally bottomed at 61.9, an all time low, losing 41 per cent of its value in the six months after the election.

1929 – Depressing Times

In the throes of the great Depression, Tory prime minister Stanley Baldwin lost his election with a “Safety First” slogan reminiscent of Theresa May’s “Strong and Stable” campaign.

Ramsay MacDonald’s minority Labour government made it through to 1931 before collapsing and being replaced by a national coalition led by Baldwin and including Conservatives, Liberals and a National Labour faction of the Labour Party.

How did investors fare? Badly. Still recovering from the 1929 Wall Street Crash, the pound was devalued by a quarter against the dollar between 1930 and 1932. Share prices bottomed in the summer of 1932.

2017 – ?

The examples above give three different possibilities for investment performance following last week’s election. Caroline Simmons, deputy head of the UK investment Office at UBS Wealth Management, says that it is difficult to compare.

“When you try to extrapolate, the numbers are not comparable,” she says.

“This time the numbers are more akin to the 1970s, but with Brexit in the equation it is hard to say what will happen.”

For investors wondering how to position their own portfolios, an expectation that the pound will remain weak for some time to come may help, she suggests.

Globally focused stocks, which tend to be larger, will do better out of a weak pound, while domestically-focused mid-cap stocks may suffer from lower consumer spending in the UK.

“We may see mid caps underperforming large caps,” Ms Simmons says. She advises clients to invest broadly in a variety of assets to try to ride out the storm.

Will there be bargains for investors?

In periods of great volatility, there are sometimes bargains available for those who invest in the stock market. David Docherty, head of UK equities at Schroders, said that domestic stocks could be sold off, but the trend could reverse quickly.

“If such a scenario were to occur again then domestic consumer stocks such as retailers could be perceived as attractively valued opportunities,” he said.

“We would highlight that, since Brexit, there has been an enormous divergence in the performance of the best and worst stocks in each sector. This demonstrates the importance of focusing on the stock level, not just on sectors.”

Hung parliaments have provided a variety of different investment scenarios, and everything depends on how quickly stability returns.

Investors need to hang on tight.

Join our commenting forum

Join thought-provoking conversations, follow other Independent readers and see their replies

Comments