Pound plummets as Kwasi Kwarteng sets out biggest raft of tax cuts for 50 years

The Chancellor abolished the top rate of income tax for the highest earners.

Your support helps us to tell the story

From reproductive rights to climate change to Big Tech, The Independent is on the ground when the story is developing. Whether it's investigating the financials of Elon Musk's pro-Trump PAC or producing our latest documentary, 'The A Word', which shines a light on the American women fighting for reproductive rights, we know how important it is to parse out the facts from the messaging.

At such a critical moment in US history, we need reporters on the ground. Your donation allows us to keep sending journalists to speak to both sides of the story.

The Independent is trusted by Americans across the entire political spectrum. And unlike many other quality news outlets, we choose not to lock Americans out of our reporting and analysis with paywalls. We believe quality journalism should be available to everyone, paid for by those who can afford it.

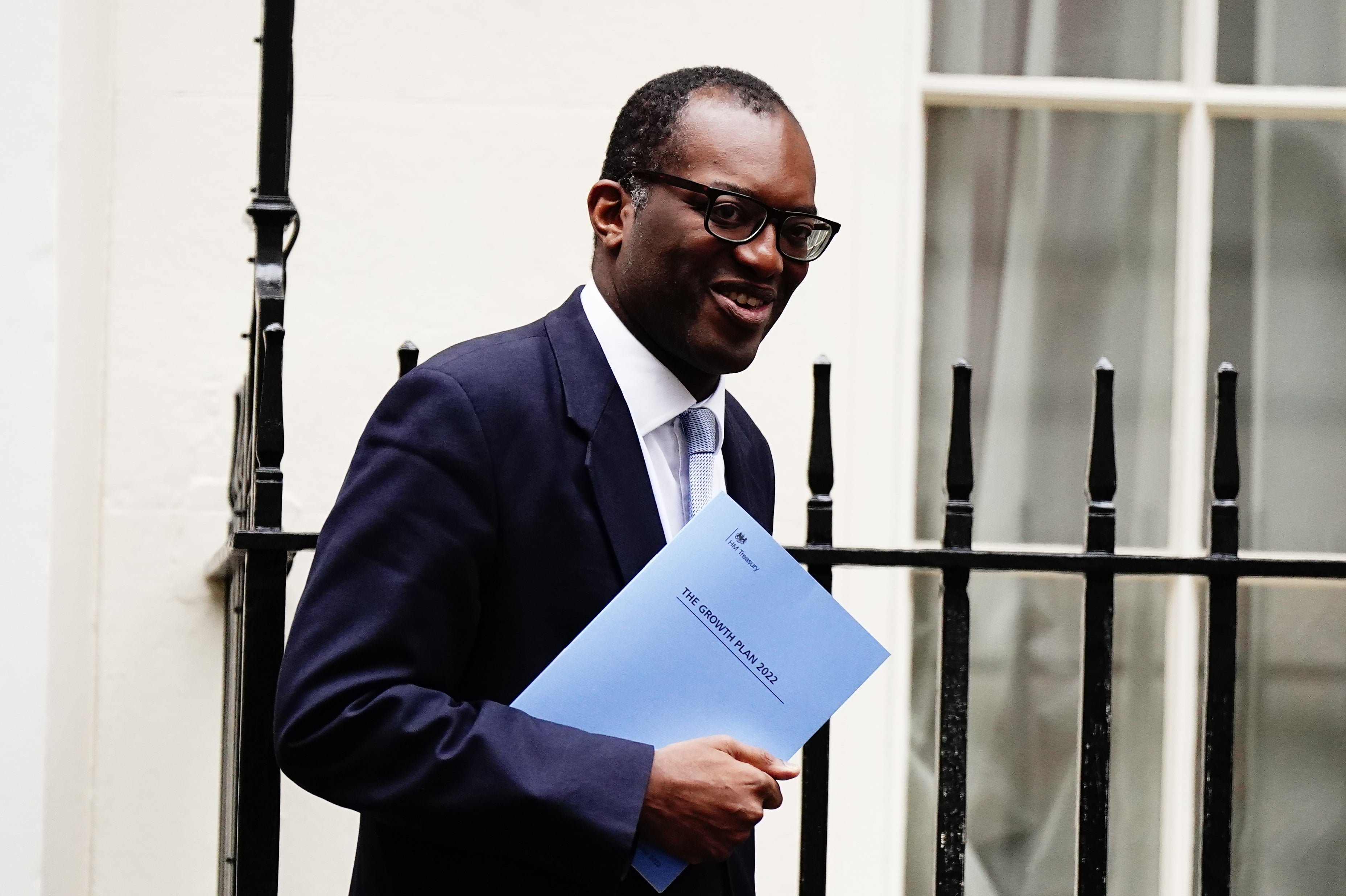

Your support makes all the difference.The pound plummeted after Chancellor Kwasi Kwarteng announced the biggest raft of tax cuts for half a century, in a “gamble” to raise falling living standards by boosting growth.

Using more than £70 billion of increased borrowing, Mr Kwarteng on Friday set out a package which included abolishing the top rate of income tax for the highest earners.

He cut stamp duty for homebuyers, and brought forward a cut to the basic rate of income tax, to 19p in the pound, a year early, to April, as part of tax cuts costing up to £45 billion annually.

Mr Kwarteng told the Commons tax cuts are “central to solving the riddle of growth” as he confirmed plans to axe the cap on bankers’ bonuses while adding restrictions to the welfare system.

But the pound dived to a fresh 37-year low as “spooked” traders swallowed the cost of the spree launched by the Chancellor and Prime Minister Liz Truss two years ahead of a general election.

The price of Government borrowing soared even higher as British bond yields rose, amid fears the package had sent the UK markets into meltdown.

Ministers were accused by the Institute of Fiscal Studies (IFS) of “betting the house” by putting Government debt on an “unsustainable rising path”.

The respected financial think tank’s scathing assessment said only those with incomes of over £155,000 will be net beneficiaries of tax policies announced by the Conservatives over the current Parliament, with the “vast majority of income tax payers paying more tax”.

Mr Kwarteng argued his economic vision with fresh deregulation will “turn the vicious cycle of stagnation into a virtuous cycle of growth”.

However, shadow chancellor Rachel Reeves said the strategy amounts to an “admission of 12 years of economic failure” under successive Conservative governments.

The Labour MP likened the Prime Minister and Mr Kwarteng to “two desperate gamblers in a casino chasing a losing run”.

Treasury estimates priced the tax cuts, including the promised reversal of the national insurance rise and axing the hike to corporation tax, at nearly £45 billion a year by 2026.

Critics questioned the fairness of the package, as the 660,000 highest earners were given an average yearly tax cut of £10,000 with the income tax change.

From April, those earning more than £150,000 a year will no longer pay the top rate of 45% and will join those on £50,271 in paying the 40% rate.

The major spending package included:

– Cuts to stamp duty in England and Northern Ireland, doubling the exemption level immediately from £125,000 to £250,000 and increasing it for first-time buyers from £300,000 to £425,000.

– An estimate that the two-year energy bills bailout will cost about £60 billion over the first six months from October.

– The planned alcohol duty hike on beer, cider, wine and spirits being cancelled, costing £600 million.

– New low-tax “investment zones” allowing planning rules to be relaxed and the reduction of business taxes to encourage investment.

– Legislation to force trade unions to put pay offers to a member vote so strikes can only be called once negotiations have fully broken down.

– Confirmation of plans to make about 120,000 more people on Universal Credit take active steps to seek more and better-paid work or face having their benefits reduced.

The package was announced a day after the Bank of England warned the UK may already be in a recession and lifted interest rates to 2.25%.

That move made Government borrowing more expensive than at any point over the past 13 years.

Paul Johnson, the IFS director, said Mr Kwarteng’s “gamble with fiscal sustainability” was the “biggest tax-cutting event since 1972”.

Amid soaring interest rates, he warned that the Bank of England will surely further hike interest rates in response to the package.

Mr Johnson said: “Early signs are that the markets – who will have to lend the money required to plug the gap in the government’s fiscal plans – aren’t impressed. This is worrying.”

Mr Johnson also warned that it was “inconceivable” that further public spending was not being announced, unless the Government will allow a “further deterioration” in public services.

“Presumably this Government would borrow for that also. Mr Kwarteng is not just gambling on a new strategy, he is betting the house,” Mr Johnson said.

Mr Johnson warned that the package of tax cuts announced 50 years ago by then-chancellor Anthony Barber under a dash for growth “ended in disaster”.

Mr Kwarteng committed to get debt falling as a percentage of GDP over the medium term, but the Treasury estimates the package would have to drive up GDP by 1% on current forecasts every year for five years to cover the cost of the new tax cuts.

The Treasury said the total package would be funded by increasing borrowing by £72.4 billion.

The IFS forecast that Government borrowing could remain as high as £110 billion a year even after the massive energy support package expires in two years, and that future tax rises or spending cuts will be needed to pay for increasing debt.

In the surprise move of what had been dubbed a mini-budget, Mr Kwarteng spent about £2 billion a year from 2025 by abolishing the top rate of income tax.

Treasury estimates say it will save the top earners £10,000 a year on average.

Torsten Bell, chief executive of the Resolution Foundation think tank, said those earning £1 million annually will get a £55,000 tax cut next year thanks to the wider package.

There was also some anxiety in the Tory party, with Treasury Select Committee chairman Mel Stride saying there was a “vast void” created by the lack of Office for Budget Responsibility forecasts.

The Chancellor avoided the scrutiny of the independent financial analysts by describing the package as a “fiscal event” rather than a full budget.

Ms Reeves said: “Never has a Government spent so much and explained so little.”

On bankers’ bonuses, Mr Kwarteng said the cap to limit them to twice salaries “never capped total remuneration”, adding: “So we’re going to get rid of it.”

Royal College of Nursing chief Pat Cullen urged members to back strike action as she called it a package that gives “billions to bankers and nothing to nurses”.

The Confederation of British Industry welcomed the package, with director-general Tony Danker saying “we have no choice but to go for growth to afford” support during the energy crisis.

However, the Joseph Rowntree Foundation said it shows the Government has “no understanding of the economic reality facing millions across the UK”.

Rebecca McDonald, chief economist at the anti-poverty charity, said: “This is a budget that has wilfully ignored families struggling through a cost-of-living emergency and instead targeted its action at the richest.”

The net cost of reversing Boris Johnson and Rishi Sunak’s 1.25 percentage point increase to national insurance imposed in April was put at about £15 billion per year.

Axing their planned corporation tax rise by maintaining it at 19% was set to come in at £18.7 billion a year by 2026.